The Joy of Missing Out

Wait and See, Waiting It Out

Thank You to Our Supporters

We want to express our sincere gratitude to everyone and especially to those who have subscribed to our Substack as paid members. While our content remains free of paywalls, the paid membership serves as a form of donation. We consider ourselves decent investors and traders but far from masterful storytellers, so your support is a meaningful affirmation of our work. We hope our insights have been helpful, especially over the past few weeks.

Market Recap: Low Probability of a V-Shaped Recovery

The market offered something for both bulls and bears last week. Over four consecutive days, we saw a 250-point decline, followed by a sharp 2%, 100-point rebound on Friday. Bulls might argue this marks a tradable short-term bottom, while bears would dismiss it as a classic dead cat bounce.

The next key level for us to watch is 5,425. A breach would increase the odds of a deeper selloff, as it would push the majority of buyers from the October 2023 lows into the red. Watching a year’s gains evaporate in just four weeks is psychologically taxing. We’ve heard of instances where spouses pressured their partners to exit positions while some gains remained, lamenting missed sales at $450 for TSLA 0.00%↑ just months ago.

Last week, we adjusted our portfolio to capitalize on volatility. On Tuesday, we rolled our primary position from 6,000 to 5,850 for the June OPEX and sold shorter-term straddles at 5,500 during the bounce, closing some 6,000 straddles. We’ll continue hedging to the upside, albeit with less urgency than a few weeks ago. For December OPEX, we hold straddles at 5,000, 5,850, and 6,000, with plans to retain the 6,000 positions as a hedge against an irrational rally or blue sky scenario.

In recent years, the worse the market gets, the louder the calls for Fed rate cuts. This hope alone can trigger significant short squeezes.

The Bigger Picture

Over the past five years, U.S. national debt has surged by 56%. The probability of printing another $8 trillion to prop up the stock market after a 10% decline, absent a major crisis, seems low. We're now experiencing the “hangover effect” of soaring interest rates and ballooning debt payments, which have doubled over the same period. We also have about 8 Trillion needed to refinance in 2025 alone.

While a short-term bottom may have formed, we aim to use any large moves to build long-term positions. We’ve yet to meet enough day-trade billionaires who consistently capture every market swing to convince us that’s a viable strategy. We’ve all tried.

What’s Changed?

1. Fundamentals Are Deteriorating: S&P 500 earnings have been quietly revised downward since the beginning of the last earnings season. Despite a 10% market decline, valuations remain stretched at 20x forward earnings. Further earnings downgrades and multiple contractions could deliver a double blow to late 2024’s rally chasers.

2. Earnings Beats Are Insufficient: Merely beating earnings estimates no longer cuts it. Companies need to deliver robust forward guidance, which is increasingly difficult amid policy uncertainty from Washington and weakening consumer confidence.

3. The D.O.G.E. Factor: Does DOGE stand for “Department of Government Efficiency” or “Dragging Our Growth Everywhere”? Similar reforms under President Clinton in the '90s caused short-term pain even it benefited the economy long-term. We’re already seeing airlines cut forecasts due to falling government travel and weak consumer demand. If DOGE executes effectively, we expect similar effects in software and other sectors to follow.

Wall Street Revises Down S&P 500 Targets

Wall Street is now cutting targets loudly:

Goldman Sachs lowered its year-end target to 6,200 from 6,500.

Yardeni Research (one of Wall Street's most prominent bulls) scaled back its “best-case” scenario to 6,400 from 7,000.

RBC Capital is flirting with its bear case of 5,775, down from 6,600.

Our Thinking

Given the current backdrop, our bias remains to the downside. It might seem foolish to stay defensive after a 10% correction, but the upside risk is limited unless we hit 6,000 in two weeks without a single down day. Data suggests a range-bound market between 5,450 and 5,750 through March for now.

We don’t believe this is 2000, but the market has over-extrapolated growth from the past two years. For us, “buying the dip” means targeting assets that had already corrected before the recent selloff and were hit again in this decline. We’ll continue accumulating cheap protection, both to the upside and downside, whenever opportunities arise.

If the narrative holds that the current administration is pressuring the Fed to cut rates, we wouldn’t be surprised to see further downside before the next Fed meeting, despite seasonality and OPEX dynamics. It’s worth noting that, the OPEX performance in recent years has been weaker than the historical average over the past 15 years or so if our memory serves us correctly.

Earnings This Week

For the week of Mar 17, 2025, notable earnings releases for companies with a market cap above $2 billion include:

2025-03-17: AM SAIC 0.00%↑ QFIN 0.00%↑ TBBB 0.00%↑ BLTE 0.00%↑

2025-03-18: AM ESLT 0.00%↑ XPEV 0.00%↑ TME 0.00%↑ BEKE 0.00%↑ FLOC 0.00%↑

2025-03-18: PM ZTO 0.00%↑ HQY 0.00%↑ STNE 0.00%↑

2025-03-19: AM GIS 0.00%↑ PUK 0.00%↑ TKC 0.00%↑ OLLI 0.00%↑ SRAD 0.00%↑

2025-03-20: AM ACN 0.00%↑ PDD 0.00%↑ LULU 0.00%↑ LEN 0.00%↑ DRI 0.00%↑

2025-03-20: PM MU 0.00%↑ NKE 0.00%↑ FDX 0.00%↑

2025-03-21: AM CCL 0.00%↑ NIO 0.00%↑

To add this FREE shared calendar, visit https://bit.ly/3ANoPtZ and click the ➕ "+" sign in the lower right corner. For iPhone, iPad, or any CalDAV device, don’t forget to enable iOS sync via https://calendar.google.com/calendar/u/0/syncselect

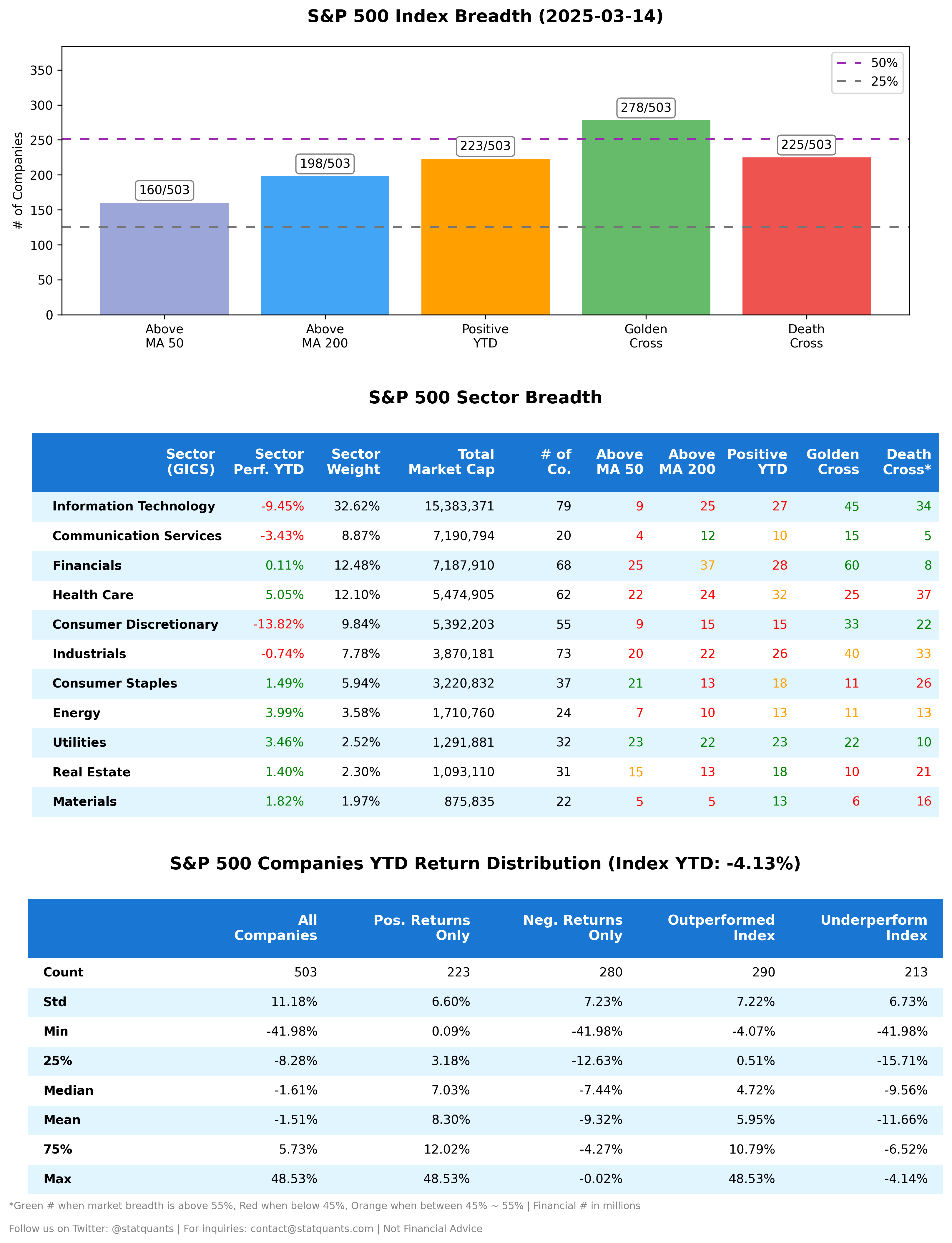

S&P 500 Sector Breadth

Information Technology

Communication Services

Financials

Consumer Discretionary

Health Care

Industrials

Consumer Staples

Energy

Utilities

Real Estate

Materials